by Paul R. Spitzzeri

Tonight, we bring the remarkable story of C.C. Julian and his Julian Petroleum Corporation to a close, mainly by focusing on the third and final part of Walter V. Woehlke’s expose on the oil promoter in the November 1927 issue of Sunset found in the Homestead’s collection.

In his concluding essay, Woehlke reiterated that Julian, who was in his late thirties when he moved to Los Angeles and launched his oil project, had failed in virtually everything he’d done and came to the City of Angels with almost nothing to his name. He was able to wring significant oil production from a quartet of wells at Santa Fe Springs and built up an aura that lured tens of thousands of investors who purchased several million dollars of “units” of stock.

When future wells failed to deliver, however, and because Julian committed to buying more property, announced he would build a refinery, constructed filling stations and expanded the scale of his enterprise, his firm began to lose value quickly. When he was forbidden to sell stock and then given a permit with limitations, it did not help his situation.

So Julian turned into attack mode, courting and creating conflict first with the state corporation commission and with federal officials and then newspapers that refused to publish his folksy and truth-stretching ads and bankers and business people for conspiring to bring him his company down.

When Julian made a deal to turn over his firm to Sheridan C. Lewis and was given a half million dollars for advances he’d made to the company, he went on lead mining and employed the same strategies of stock selling and fighting authority figures. By the time, Woehlke penned his devastating critique, Julian had three consecutive firms (Western Lead, Julian Merger Mines and New Monte Cristo Mining) that tried and failed to duplicate the success, short-lived and unsustainable as it was, he’d scored with “Julian Pete.” Again, he blamed others.

As for Lewis, he proved to be more politic, wily and adept at attracting major business and banking figures, at merging with a viable oil company, and at acquiring a legitimate stock brokerage firm—all of this gave the appearance of stability and solidity, even as Lewis’ young colleague, Jake Berman, developed a remarkable stock producing and selling scheme that raised huge amounts of money, but on large false pretenses. This also violated the limits on stock sales and distribution of funds imposed by the state.

So, in May 1927, Julian Petroleum Company, then under the name of California-Eastern Oil Company, went belly up. Lewis tried to manage the crisis and Julian saw an opportunity to resurrect his ragged fortunes by going on the attack again. He accused bankers, film luminaries and others of seeking profit at the expense of his company and used the radio as a prime tool for launching the invectives.

To Woehlke, this looked to be a success, especially after District Attorney Asa Keyes, whose 1924 election campaign was openly supported by Julian, finally convened a grand jury, which indicated dozens of figures, such as banker Motley Flint, movie producer Louis B. Mayer, and conservative power broker Harry Haldeman (son of President Richard Nixon’s chief of staff.)

The author observed that bankers were encouraged and saw value in the idea that

if they use money entrusted to them by the depositors to finance crazy ventures, to encourage speculation and unwise expansion, if they hire out the money carelessly at excessive wages and with insufficient security to guarantee its return, then the entire community suffers on the day of reckoning.

This sounded a great deal like what happened a half-century before to the Temple and Workman bank and what would transpire a little under than two years later when the New York stock market crashed and sent the nation and the world plummeting into the unremitting depths of the Great Depression.

The massive growth of Los Angeles in the first twenty-five years of the 20th century, however, required that its bankers move away from conservatism in loaning policy, Woehlke went on, and demonstrate faith in the city’s development by putting capital out there through loans. This, though, meant that the financial leaders of the region “had to have judgment and backbone enough to hold speculation within reasonable bounds, to check it entirely, if necessary.”

While the rise of the motion picture, agriculture, real estate and oil industries were handled with reasonable loaning and investment policies, then conditions were generally acceptable and even laudable. Woehlke noted that he’d predicted, within a month, the collapse of the last real estate boom in 1924 (not long after Walter P. Temple launched his biggest development project, the Town of Temple, renamed Temple City in 1928). He also observed that bankers and other financial leaders managed the bust in a way that minimized the negative effects.

Yet, when Pacific Southwest Trust and Savings Bank and the First National Bank of Los Angeles loaned money to Julian through Lewis’ ministrations, the writer opined, they did so with the best of intentions to build the firm through legitimate means so that it would become a stable, sustainable business (and, of course, bring reasonable profits to them). Julian, in a more vehement way, and Lewis, more quietly, claimed otherwise and the grand jury’s mass indictment list was stunning.

It was true that in the May 1927 failure of Julian Pete, the business owned $11 million, most of it secured by properties and other assets, but there was $2 million that was loaned to Lewis with only “the general credit of the company as the only security.” This reflected how successfully Lewis seduced the powerful financial figures in these banks.

Again, when Lewis acquired A.C. Wagy and Company and its estimate stock brokerage portfolio and worked a deal with Pacific Southwest Trust and Savings to pour funds into the newly merged firms of Julian Pete and Marine Oil, it looked like reasonable and responsible actions to improve the situation.

Behind the scenes, however, Berman and associates were busily printing more stock than allowed by permit, manipulating prices through Wagy and Company and other means,and engaging in creative ways to develop income through stock pools, reinvested profits back to the company rather than to investors’ pockets, and stock price manipulation. When the question of stock over issue arose, though, Lewis claimed the additional securities were done on his own advances of $6.5 million.

While the argument seemed plausible, the responsible thing to do for the bankers who’d poured large sums into the concern was to ask for an audit of the books, which were conveniently removed by Lewis to New York. Lewis tried to argue against an audit and stalled and delayed as long as he could. Even as the audit took place, he still maintained the faith and trust of most of those involved.

Finally, on 6 May 1927, the shattering news came out that, while there was the limit of 600,000 shares imposed by the corporation commission, Berman and his cronies had instead issued over 3.6 million to the tune of over $33 million. Add to that $11 million in bank loans and some $2 million in Wagy and Company profits and there was a heft amount of receipts.

By Woehlke’s accounting, about $20 million was in legitimate expansion efforts and another $5 million went toward countering large deficits, but that left about $21 million that was unexplained. Moreover, as the heat was on, Berman skipped town for Paris and other European points and allegedly had $625,000 in cash in a belt when he did so. Lewis was said to have $500,000 in cash from a safe deposit box that he claimed was to be used to “establishing a market for California Eastern” stock.

Even if there were a few million dollars stashed away elsewhere, that left many millions that went to commissions, bonuses and interest on questionable stock sales and loans. Woehlke wrote that Berman was not on the payroll of either Julian or Wagy, but used both firms to build his massive scheme, assisted by a host of colleagues and entered into transactions with massive sums to the benefit of himself and Lewis, but to the great detriment of stockholders and virtually anyone else associated with the companies.

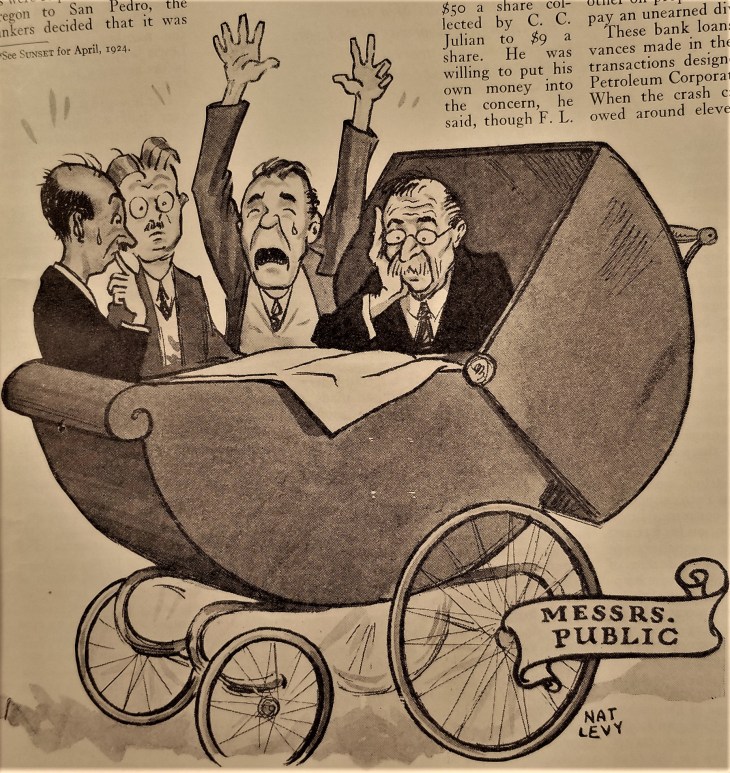

Motley Flint, vice-president of Pacific Southwest and brother of a U.S. Senator from California, got wind of Berman’s shady and shadowy role in the enterprise, and tried to induce Lewis to address the mounting problems. Craftily, Lewis induced Flint to join in an enormous stock pool that was structured to look like it would address the growing issues of the situation.

Sure enough, stock prices rallied and Lewis looked like a genius, but, when his partners and investors asked him to sell the stock and distribute the dividends, he said no, claiming it would unduly affect the market. He asked shareholders in the pool to wait a month and then he would pay them a profit of $3 a share regardless of what the market did.

Notably, investors in a San Francisco pool refused to do what their Los Angeles counterparts did and many of the latter were indicted for their willingness to placate Lewis and for transferring monies to a hastily organized subsidiary company and using the funds to reduce the amount owned by Julian Pete to Pacific Southwest. This had all the earmarks to the grand jury of embezzlement, though Woehlke claimed that C.C. Julian’s ratcheted-up radio rhetoric was directly responsible for the grand jury indictments.

Meanwhile, Lewis and Berman blamed each other for the manifold schemes of the Julian Pete scandal, though, of course, both were neck-deep in responsibility for the disaster, as outlined in Woehlke’s article and in this post. Lewis found ways to continue the misleading of investors of all kinds, including the rich and powerful as well as the small and medium size shareholders.

Perhaps, the writer went on, Lewis turned a blind eye to Berman’s methods or thought a solution would somehow arise. Maybe there was a point when Lewis could do nothing and Berman operated with a free hand. Or, it was also possible that the former was perfectly aware of what the latter was doing and was directly involved in the dirty details.

Woehlke concluded that the questions “will perhaps be cleared up in the trial of Lewis on the various charges against him,” though he also noted that “the law is full of loopholes” in “a jungle of technicalities.” He also observed that

Legal talent of a high order possessed of a grim determination will be required to convict anybody in the Julian Pete scandal.

With all the damage done through losses to stockholders, jobs sacrificed and in other ways, Woehlke added that

The Julian Pete mess has demonstrated that California’s Blue Sky needs bigger and better teeth, that the officials entrusted with the enforcement of the law need more and better cooperation from the prosecuting attorneys. It has also demonstrated the need of a house-cleaning in the stock exchanges, followed by state regulation and supervision of these private institutions. And it has shown that the safeguards thrown around the issuing of stock certificates are inadequate and must be improved.

These are prescient words for 1929, as well as for 1987, 2008 and whenever the next financial disaster hits.

A trial was held in the first part of 1928, though charges were dropped against everyone but Lewis, Berman and five other Julian employees and associates. As Woehlke said, though, it required the best of the legal system to get convictions secured and there was great shock and anger when the jury found all seven innocent. A jury member simply said that the county’s case was badly insufficient.

Not surprisingly, it was later learned that Asa Keyes, so assiduously supported by C.C. Julian in the 1924 election, was bribed by Lewis to water down the case. Keyes did not run for reelection, but shortly after he left office he was indicted. In February 1929, the disgraced former DA was convicted of criminal conspiracy and he was sentenced to a term of 1-14 years at San Quentin, though the parole board set a term of five, three in prison and two on parole. With good behavior credits, Keyes got out in October 1931 and worked in bail bonds and selling cars. After he was pardoned by the governor in 1933, an effort to reinstate his license to practice law was mounted, but Keyes died the next year of a stroke.

Motley Flint was a witness in a civil trial involving his bank and film impresario David O. Selznick when Frank Keaton, a Julian Pete investor who’d lost his hard-earned money in the 1927 debacle, suddenly rose, put his hat over a pistol and fired three shots, all taking effect in Flint’s body and killing him.

Sheridan Lewis, who walked out of court in spring 1928 a free man, was tried and convicted in federal court for mail fraud later that year but appealed for a lengthy period and did not begin his sentence on McNeil Island in Washington until April 1930. His term was for seven years but he was released, with credits for good behavior, in July 1935. After returning to Los Angeles for a few years, he returned to Texas, where the Alabama native once practiced law before getting into oil and he continued to work in the latter in Corpus Christi. He lived until 1972, living to be 82 years of age.

Julian, meanwhile, decamped to Oklahoma, formed an oil company largely on the same model of operations as he’d practiced in California, and was forced out of business under threat of legal action. He hightailed it out of the country and landed in Shanghai, where he committed suicide in March 1934, months before Keyes’ early demise.

The story of C.C. Julian and his Julian Petroleum Company is easily one of the most notorious business scandals in Los Angeles history and was the subject of a 1929 book by Los Angeles journalist Guy Finney called The Great Los Angeles Bubble and Jules Tygiel’s 1994 work, The Great Los Angeles Swindle.

2 thoughts