by Paul R. Spitzzeri

Walter P. Temple, the highly fortunate beneficiary of a small fortune derived from 1917 onward from oil found on his Montebello-area ranch by his young son, Thomas, worked with his friend and business manager, Milton Kauffman, to move into real estate development within a couple of years.

As greater Los Angeles embarked on another of its succession of population and building booms in the very early 1920s, the two were well-positioned to take advantage of opportunities with projects in Alhambra, downtown Los Angeles, San Gabriel, El Monte and, in spring 1923, the formation of the Town of Temple, renamed Temple City in 1928.

There was a deeply personal motivation for Temple, as well, because the 285 acres he acquired from a company that was planning a subdivision there was formerly owned by his father, F.P.F. Temple, and his grandfather, William Workman, when they were partners in the western two-third of Rancho San Francisquito with Lewis Wolfskill, whose father-in-law, Henry Dalton, long owned the ranch.

The establishment of the town was publicized as a way to memorialize the Temple and Workman families, as well as a way to, hopefully, reap a windfall in profits. While “location, location, location” is an understandable platitude about real estate, so is “timing, timing, timing.” In 1923, after a few years of red-hot activity, the real estate market peaked and began a downward trend, so the inauguration of the Town of Temple was a bit late to ride a wave.

Another issue is the rapidity with which Temple embarked on his development projects. His first completed endeavor was the Temple Theater, a movie house in Alhambra that opened in late December 1921, and within a year-and-a-half, up to the time the news about the Town of Temple founding was released, he started or finished projects in San Gabriel and El Monte and was readying to join a syndicate to built two office structures in downtown Los Angeles.

Whatever revenues were to accrue from rentals and leases for stores and offices had to be juxtaposed, naturally, with liabilities through mortgages, interest payments and other obligations for purchases through trust agreements, loans, and other expenses. The excitement of boom times was due to the powerful lure of ambitions to make money quickly, but becoming over-extended was a particularly worrisome risk.

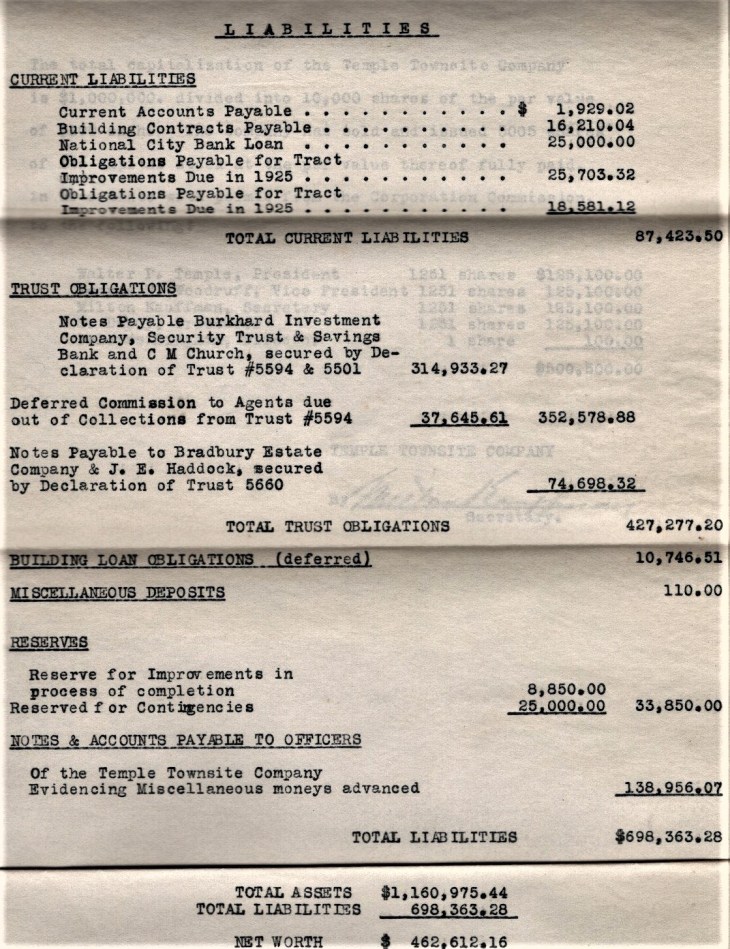

While the Homestead’s collection does not have a complete archive of Temple’s business papers, there are artifacts that help us get an understanding of how his endeavors evolved over the course of the 1920s. This includes today’s featured object, an asset and liability statement as of 1 August 1925 for the Temple Townsite Company, the firm organized to manage the development of the Town of Temple.

As noted on the last page of the three-page document, the company’s capitalization was $1 million with 10,000 shares of stock at a par value of $100 each. To date, the statement noted, “the company has sold and issued 5005 shares of its capital stock at the par value thereof fully paid, in accordance with [the] permit from the [state] Corporation Commission.”

The issuance of stock was divided evenly among the principal partners: firm president Temple, its secretary Kauffman, Temple’s lawyer and company Vice-President George H. Woodruff, and Sylvester Dupuy, who was treasurer and who was soon to finish his “Pyrenees Castle” in Alhambra and which became (in)famous when its later owner, record producer Phil Spector shot and killed Lana Clarkson in the home in 2003.

Each of the quartet held 1,251 shares with the obvious value of $125,100, while Dolores Bingham, who the secretary at the townsite company office, was given a sole share, because state law required that there be at least five directors for any incorporated company.

With respect to current assets, the statements listed first lien mortgages of just over $484,000 and first lien contracts of $120.000, these being with parties who bought property or had other obligations with the townsite. There were smaller amounts of money trust deeds, interest receivable and accounts and notes receivable, these totaling under $50,000. Perhaps most notable is the cash amount of just above $13,000, as this appears to be a low amount to have on hand. The total of current assets was listed as $660,000.

Also listed as an asset, but not delineated specifically, was “Stocks in Other Companies” of some $45,000, and it would be interesting to know why the townsite company would own stock in other companies. Office equipment, furniture and machinery and automobiles owned by the firm comprised just under $4,200.

Real estate owned by the company comprised the second largest amount in the asset category, including 345 lots in the town with a valuation of $445,000, though the selling commission of 15% brought that figure down to $378,000. There wasn’t much improved property owned by the company so that total was a bit under $35,000, though that was subject to first mortgage loans of $15,000, leaving about $20,000.

Then, there were two other properties listed as owned by the company and, again, one wonders why these were held under that firm as opposed to Temple’s Temple Estate Company, which owned and developed all of his other real estate projects. The Mission Manor Tract was located in the City of San Gabriel, and, not surprisingly, was located just southeast of the Mission San Gabriel off Del Mar. The firm owned eighteen lots there valued at $13,050—later Walter’s son Thomas lived in that area of town, though it is not known if he acquired a lot once owned by his father’s firm. The other property was shown as “Antelope Valley Ranch” and was deemed worth $16,000, though it is unknown where in the remote area near Lancaster and Palmdale the property was or why it was an asset of the townsite company. Total real estate assets were valued at nearly $427,000, for an overall asset determination of $1,160,975.44.

On the liabilities page were current liabilities of over $87,000, about half of which were obligations for improvements made at the townsite in 1925, though there was no explanation of why this was divided into two sums of roughly $26,000 and $19,000. There was a loan from the National City Bank, which had its headquarters in one of the two Los Angeles office buildings built by a syndicate including Temple, Kauffman and Woodruff, who was a director, and totaling $25,000. Payable building contracts totaled about $16,000 and there was a little under $2,000 for accounts payable.

The biggest liability by far was obvious, these being notes payable under the Trust Obligations section to the Burkhard Investment Company, Security Trust and Savings Bank, and C.M. Church, and covered, along with deferred agent commissions, by two Declarations of Trust totaling over $350,000. The Burkhard Investment Company, which had oil property and also developed tracts in Santa Monica and Hemet, bought the Rancho San Francisquito tract years prior to its 1922 announcement that it would develop “Sunny Slope Acres” on it.

In addition, there were noted payable to J.E. Haddock and the Bradbury Estate Company for just under $75,000. The latter firm was formed by Louis Bradbury, a remarkable figure who built the famed and unique Bradbury Building in downtown Los Angeles in the late 19th century and whose San Gabriel Valley ranch later became the exclusive and tony City of Bradbury above Duarte. Total trust obligations amounted to nearly $430,000.

Another major chunk of the liabilities comprised almost $140,000 listed as “notes & accounts payable to officers of the Temple Townsite Company evidencing miscellaneous moneys advanced.” Again, there was no detail provided and the wording is interesting and, perhaps, concerning, as these funds amounted to 20% of all liabilities.

There were reserves of almost $34,000, with $25,000 being “reserved for contingencies,” as almost a supplement to the cash on hand, while just under $9,000 was for reserve for improvements underway in the town. Finally, there were deferred building loan obligations of almost $11,000 and a small sum of $110 of miscellaneous deposits.

The grand total of obligations was just shy of $700,000 and compared to the declared assets of about $1,161,000, the surface level view was of a reasonably healthy company showing a net worth of not far south of a half million dollars. Again, though, about 3/4 of the assets were for the nearly 350 undeveloped lots in town and first lien mortgages, presumably for lots that were sold and financed by the company.

A major concern with the unsold lots was two-fold. First, would real estate prices continue to drop as the boom eased? Second, the unincorporated town was subject to an assessment called the Mattoon Act, which was well-intended in trying to fund improvements like gas lines, sidewalks and street lights, but had a provision that defaulting assessments of a property owner were to be shared by the neighbors around that property. This had a major effect on sales of lots in these communities, including the Town of Temple.

In fact, within in a year, Temple and his associates decided to issue bonds, covered in a previous post here, to try to refinance the Town of Temple project and get it onto a solid economic footing. With the Mattoon Act scaring prospective buyers and settlers away, the real estate market softening, and Temple’s own precarious financial position worsening, the bond issue did not solve the problems the town faced.

By the end of the decade, the situation was dire and, as Temple divested himself of other properties managed by the Temple Estate Company, he finally reached a deal in spring 1930 to sell his Temple City holdings to a new firm, the Temple City Company, which included the original Town of Temple sales agent, Marsh and Coughran, as among the principals.

That May, Temple moved from the Homestead to Ensenada, in Baja California, because he’d leased the ranch to the Golden State Military Academy of Redondo Beach and to save money while he desperately tried to save that last piece of his estate. By summer 1932, however, even that was not possible and the Homestead was lost to a bank foreclosure.

Temple City, however, survived and, though it was largely stagnant through the Great Depression and World War II, it grew during the postwar boom and was incorporated in 1960. It has long been a desirable suburban bedroom community and will celebrate its centennial in three years. This statement is a notable document from the Homestead’s collection about the early history of Temple City and its financial situation.